登入 國立政治大學商學院

| 2024-02-21 | 重要 熱門 政大商業評論2024上半年度徵稿公告 | 重要 學術活動 熱門 學術活動 學術活動 |

| 2023-11-15 | 重要 熱門 [博士班] 英文寫作研習課程公告 | 重要 學術活動 熱門 學術活動 學術活動 |

| 2024-02-07 | 熱門 112學年度第2學期商學院重要學術研究補助公告_(教師/學系) | 熱門 學術活動 學術活動 |

| 2024-01-04 | 熱門 113年度商學院潛力教師國際合作徵件計畫 | 熱門 學術活動 學術活動 |

| 2023-12-19 | 共創永續未來 企業永續管理研究中心研討會 | 學術活動 |

| 2023-11-02 | 前瞻綠色金融淨零投資趨勢 共創ESG永續未來 | 學術活動 |

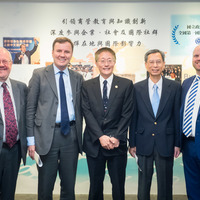

| 2023-03-17 |

熱門

政大攜手五校與中信金控合作共同開設金融科技課程 |

熱門 學術活動 學術活動 |

| 2023-02-24 |

熱門

商學院創新創業學程代表隊榮獲金融時報責任商管教育獎肯定 |

熱門 學術活動 學術活動 |

| 2022-11-18 | 熱門 政大舉辦首屆DBA高峰論壇 解析企業永續的關鍵思維 | 熱門 學術活動 學術活動 |

| 2022-02-25 | 熱門 政大商學院2022年度DBA畢業典禮,蔡維奇院長期望畢業生為國家社會與產業發展帶來正面影響力 | 熱門 學術活動 學術活動 |

| 2024-04-12 | 重要 熱門 國立政治大學商學院內補徵才公告(預估缺) | 重要 徵才訊息 熱門 徵才訊息 徵才訊息 |

| 2024-04-12 | 重要 熱門 國立政治大學商學院外補徵才公告(預估缺) | 重要 徵才訊息 熱門 徵才訊息 徵才訊息 |

| 2024-03-11 | 重要 熱門 國立政治大學商學院金融科技研究中心甄才公告 | 重要 徵才訊息 熱門 徵才訊息 徵才訊息 |

| 2024-04-22 | 熱門 【商學院徵才說明會】妮維雅實習生計畫×Adecco | 熱門 徵才訊息 徵才訊息 |

| 2024-04-22 | 熱門 【商學院徵才說明會】2024年亞洲發展新契機×國泰人壽 | 熱門 徵才訊息 徵才訊息 |

| 2024-04-18 | 熱門 【商學院徵才說明會】Hi-P徵才說明會 | 熱門 徵才訊息 徵才訊息 |

| 2024-04-17 | 112學年第2學期Amundi實習生錄取名單公告 | 徵才訊息 |

| 2024-02-02 | 熱門 【商學院徵才說明會】永豐金控_Turing Plan_百萬年薪 儲備AI科學家 | 熱門 徵才訊息 徵才訊息 |

| 2024-02-02 | 熱門 【商學院徵才說明會】南山人壽儲備菁英與實習生計畫 | 熱門 徵才訊息 徵才訊息 |

| 2024-01-19 | 熱門 【徵才】兆豐證券-國際業務開發人員、新金融商品開發及交易人員 | 熱門 徵才訊息 徵才訊息 |

| 2023-11-28 | 熱門 【112學年度大一新生親師座談會】赴會通知 | 熱門 招生訊息 招生訊息 |

| 2023-08-14 | 熱門 2023政大商學院英語商管專班(ETP)申請說明 | 熱門 招生訊息 招生訊息 |

| 2023-03-01 |

熱門

112學年度《博士班招生》於112年3月14日上午9時起至3月28日下午3時止 開放報名 |

熱門 招生訊息 招生訊息 |

| 2019-12-27 | 2020 NCCUC Doctoral Programs Fall International Admission Intake | 招生訊息 |

| 2016-04-13 | 【講座/從廣告案例看品牌價值】 | 招生訊息 |

| 2015-08-19 | 國立政治大學商學院【大一新生院系迎新】重要報名資訊 | 招生訊息 |

| 2024-04-01 |

重要

熱門

113學年度第1學期「希望起飛出國交換奬學金試辦計畫」即日起開放申請,至5月9日截止! |

重要 獎助學金 熱門 獎助學金 獎助學金 |

| 2024-03-04 | 重要 熱門 112學年第2學期【Amundi鋒裕匯理投資創新獎學金】申請公告 | 重要 獎助學金 熱門 獎助學金 獎助學金 |

| 2023-09-27 | 重要 熱門 [獎學金] 113學年度國科會甄選博士班新生獎學金申請至112/10/16截止 | 重要 獎助學金 熱門 獎助學金 獎助學金 |

| 2020-12-15 | 重要 政大商學院僑生及港澳生新生獎助學金相關規定 | 重要 獎助學金 獎助學金 |

| 2024-04-02 | 【2024印尼梁世烈獎學金】即日起開放申請,至2024/04/30(二)截止 | 獎助學金 |

| 2024-03-26 | 【2024陳思明先生與趙新民女士紀念獎學金】即日起開放申請,至2024/04/30(二)截止 | 獎助學金 |

| 2024-02-19 | 熱門 2024秋季商學院【明門海外學習獎學金】申請公告 | 熱門 獎助學金 獎助學金 |

| 2024-02-02 | 【112-2 萬海慈善育才助學金】即日起開放申請,至2024/03/01(五)截止 | 獎助學金 |

| 2023-12-25 | 【112學年第1學期 Amundi鋒裕匯理投資創新獎學金】獲獎名單公告 | 獎助學金 |

| 2023-11-30 | 【112-1萬海慈善育才助學金】獲獎名單 | 獎助學金 |

| 2023-02-23 | 重要 企業最愛大學生排行榜,政大連續第六年拿下文法商領域三冠王 | 重要 其他 其他 |

| 2024-03-15 | 【2024 Back to School 開學週】「好禮天天抽」得獎名單 | 其他 |

| 2024-02-26 | 【2024 Back to School 開學週】掌握學習資源×領取美味輕食×參加好禮抽獎! | 其他 |

| 2023-10-11 | 熱門 112學年度 (2024 Spring)希望起飛出國交換獎學金試辦計畫獎學金申請自即日起至10月19日下午5:00止! | 熱門 其他 其他 |

| 2023-07-19 |

熱門

本院暑假上班時間調整異動通知(2023/7/17- 8/18期間) |

熱門 其他 其他 |

| 2023-04-21 | 熱門 【05月12日】政大USR計畫|《稻浪上的夢想家》電影特映會 | 熱門 其他 其他 |

| 2022-11-11 | 【2022 政大商學院Back to School開學週】滿意度問卷得獎名單 | 其他 |

| 2022-04-19 | 【商學院職涯講座】世界級的動畫軟體公司居然在台灣?5月12日歡迎加入甲尚科技國際化創新競技場 | 其他 |

| 2019-11-29 | 臺灣微軟攜手政治大學開辦《AI商學院》 | 其他 |

| 2019-11-29 | 108學年度政大商學院大一新生親師座談會 | 其他 |